Build an Income Machine, Not a Withdrawal Strategy

MP Market Review - June 9, 2026

Summary

This is not a stock-picking newsletter.

It’s a behind-the-scenes look at how a dividend growth portfolio is built, maintained, and improved over time.

Welcome to this week’s MP Market Review. Each week, we track the Canadian dividend growth companies on The List, our curated watchlist of businesses designed to produce rising income. While we also publish a U.S. edition monthly, Canada remains our training ground.

Our objective is simple: grow dividend income by 7–10%+ annually while delivering capital appreciation that matches or exceeds the TSX Composite in Canada and the S&P 500 for our U.S. investors over a full market cycle.

What you’re about to read isn’t theory. It’s the real-time application of a dividend growth strategy using real money, with a clear objective: growing income first and letting capital growth follow.

Markets generate a lot of noise. We ignore most of it.

Instead, we track a small set of metrics that tell us whether our dividend growth strategy is working in real time. No forecasts. No opinions. Just results.

Here they are:

Dividend income from The List: +6.6% year-to-date

Capital value: +5.2% year-to-date

Dividend announcements last week: None

Earnings reports last week: None

Earnings reports this week: One

DGI Clipboard

“The safest withdrawal rate is the dividend yield.”

- Lowell Miller

Build an Income Machine, Not a Withdrawal Strategy

I was having drinks with a friend last week when he told me he had just met with a financial planner.

The planner showed him that, based on the capital he has saved today, he could enjoy a comfortable retirement using a 4% withdrawal strategy.

I have to admit, I was a little surprised.

Not because the math doesn’t work, but because financial professionals still rely on the 4% Rule as the foundation of their retirement planning.

The 4% Rule dates back to research conducted in the 1990s. The idea is straightforward. In your first year of retirement, you withdraw 4% of your portfolio. Each year thereafter, you increase that withdrawal by the rate of inflation. Historically, a diversified portfolio of stocks and bonds had a reasonable chance of lasting for at least 30 years using this approach.

The hope is that investment returns replenish the reservoir quickly enough that you never run out.

The problem with most retirement withdrawal strategies (including the 4% Rule) is that they depend heavily on the price of stocks at the exact moment you need to sell them.

What happens if the market declines 20%, 30%, or even 40% just before you retire?

Even worse, what if those poor returns occur during the first few years of retirement?

Financial planners call this sequence-of-returns risk. Two retirees can earn the exact same average return over retirement and end up with dramatically different outcomes depending on when those returns occur.

If you are forced to sell shares during a market downturn to fund your lifestyle, you permanently reduce the number of income-producing assets you own. Fewer shares mean less participation in the eventual recovery. The damage can be difficult to reverse.

Dividend growth investing approaches retirement differently.

Instead of relying primarily on asset sales, the focus is on building a portfolio of high-quality companies that pay reliable, growing dividends. The goal is to live increasingly off the cash flow generated by the portfolio rather than the sale of the portfolio itself.

When markets decline, dividends from quality companies tend to be far more stable than share prices. While prices can fluctuate wildly from year to year, many dividend growers continue to raise their dividends through recessions, bear markets, and periods of uncertainty.

This creates an important psychological advantage for retirees.

When your income continues arriving regardless of market headlines, you are less likely to panic and less likely to sell assets at precisely the wrong time.

Think of it this way.

Traditional withdrawal strategies ask investors to spend their capital.

Dividend growth investing encourages investors to spend the income generated by their capital.

That distinction may seem subtle, but over a retirement that lasts twenty or thirty years, it can make a meaningful difference.

This is why we focus so much on building an income machine.

Not because market prices don’t matter.

They do.

But when retirement arrives, it is comforting to know that your lifestyle is supported by a growing stream of dividend income rather than the unpredictable mood swings of the stock market.

Takeaway

The best retirement plan isn’t one that depends on selling shares.

It’s one that allows you to keep owning them.

Looking for a helping hand in the market? Members of Magic Pants Dividend Growth Investing get exclusive ideas and guidance to navigate any climate.

The Magic Pants model portfolios (Canadian and American) are real-money, dividend-growth portfolios funded with actual capital and executed in live accounts. Every position shown is owned, sized, and tracked in real time using our disciplined DGI process.

Become a PAID subscriber, and I’ll show you exactly how I do it. In addition, gain full access to this post and exclusive, subscriber-only content. We do the work; you stay in control!

DGI Scorecard

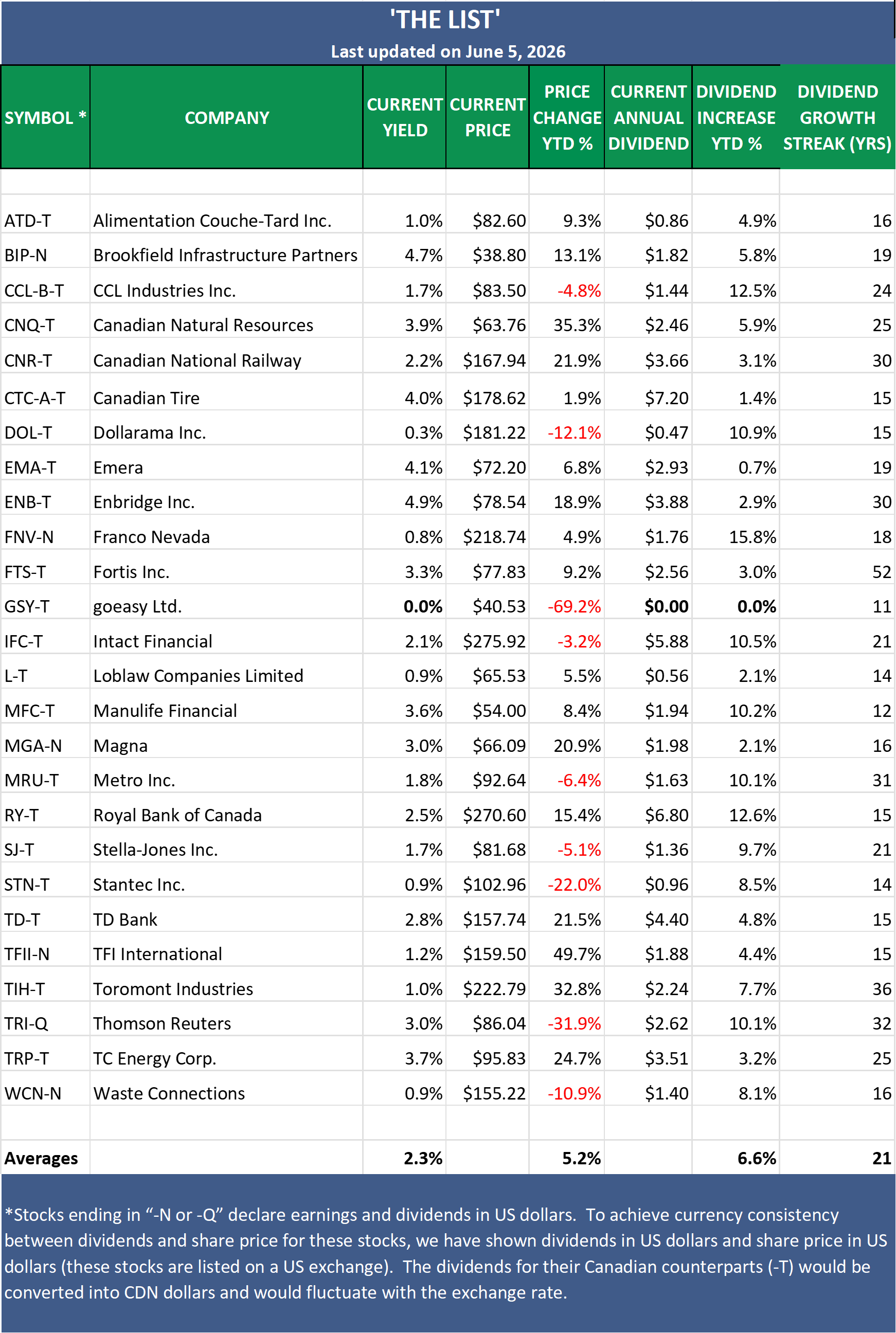

The Magic Pants 2026 list (The List) includes 26 Canadian dividend growth stocks, and our new American watchlist (The List-USA) contains 28 companies. Here are the criteria to be considered a candidate on our watchlists:

Dividend growth streak: 10 years or more.

Market cap: Minimum one billion dollars.

Diversification: Limit of five companies per sector, preferably two per industry.

Cyclicality: Exclude REITs and pure-play energy companies due to high cyclicality.

Based on these criteria, companies are added or removed from ‘The List’ annually on January 1. Prices and dividends are updated weekly.

‘The List’ is not a portfolio but a coaching tool that helps us think through ideas and manage risk in our model portfolio. We own some, but not all, of the companies on ‘The List’. In other words, we might want to buy these companies when the valuation looks attractive.

Our newsletter provides readers with a comprehensive insight into the implementation and advantages of our dividend growth investing strategy. This evidence-based, unbiased approach empowers DIY investors to outperform both actively managed dividend funds and passively managed indexes and dividend ETFs over longer-term horizons.

Note: In the last week of every month, I will show the updated watchlist for our American dividend growers, The List-USA. It will be shown after the Canadian watchlist below.

Performance of 'The List'

The dividend growth for The List remained unchanged last week, with an average YTD increase of 6.6% (income).

The price of The List was up last week and now stands at +5.2% YTD (capital).

Top Performers Last Week:

Loblaw Companies Limited (L-T), up +6.26%.

Alimentation Couche-Tard Inc. (ATD-T), up +6.05%.

Stella-Jones Inc. (SJ-T), up +5.60%.

Worst Performer Last Week:

CCL Industries Inc. (CCL-B-T), down -6.22%.

From breaking news to quarterly earnings reports, we break down the week’s biggest headlines to help you make sense of the market.