Ignore the Noise, Trust the Process

MP Market Review - May 23, 2025

Summary

Welcome to this week’s MP Market Review – your go-to source for insights and updates on the Canadian dividend growth companies we track on The List! While we’ve expanded our watchlists to include U.S. companies, The List-USA, our Canadian lineup remains the cornerstone of our coaching approach.

Don’t miss out on exclusive newsletters and premium content that will help you sharpen your investing strategy. Explore it all at magicpants.substack.com.

Your journey to dividend growth mastery starts here – let’s dive in!

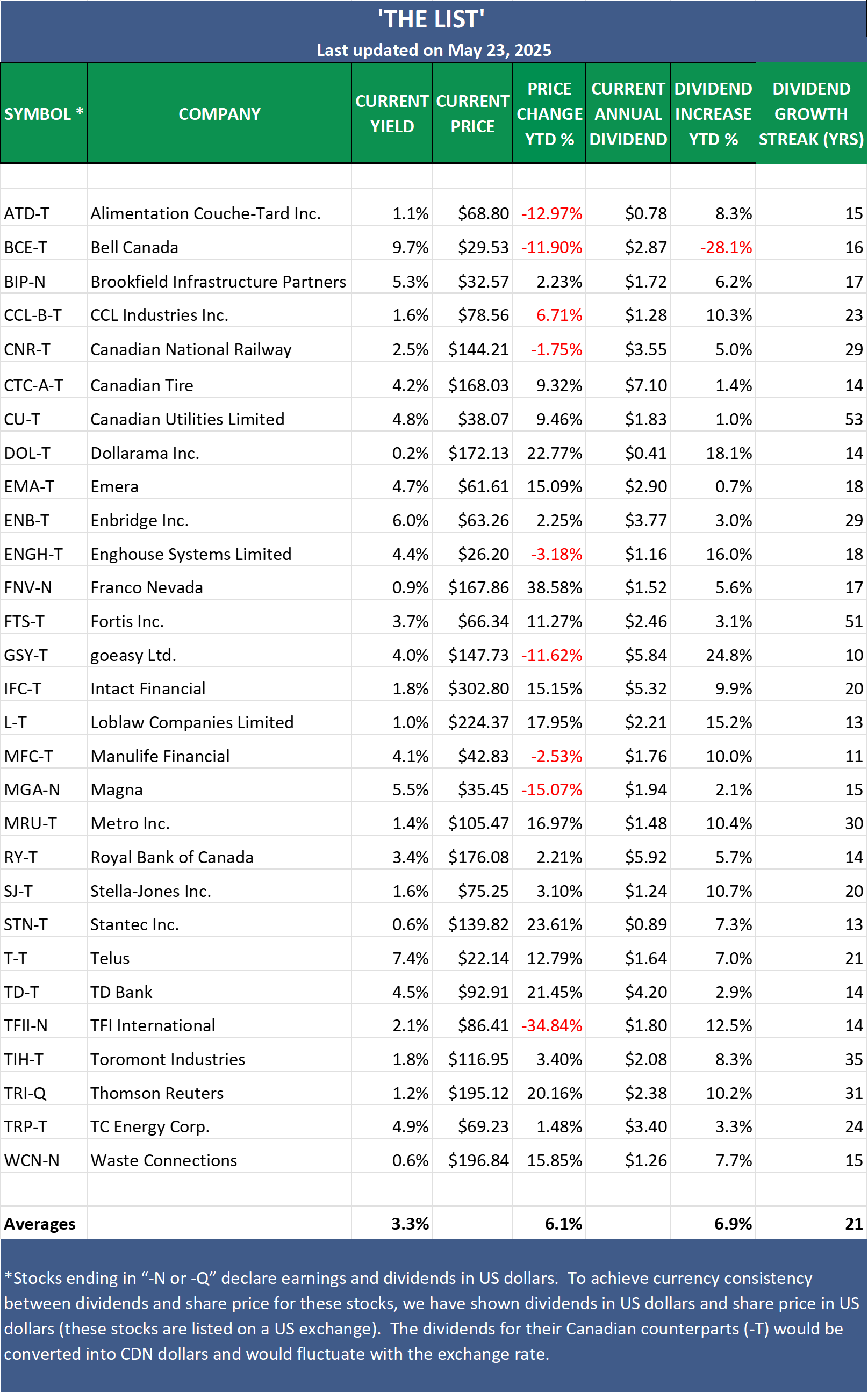

Last week, dividend growth stayed the same with an average return of +6.9% YTD (income).

Last week, the price of The List was up from the previous week with an average return of +6.1% YTD (capital).

Last week, there were no dividend announcements from companies on The List.

Last week, there was one earnings report from a company on The List.

This week, one company on The List will report on their off-cycle earnings.

DGI Clipboard

“patience is a virtue that carries a lot of wait.”

- Unknown

Ignore the Noise, Trust the Process

Intro

Later this week, I’ll be sharing our quarterly review summary for both the Canadian and American model portfolios.

One of the key themes we’ve emphasized this year is how our dividend growth companies tend to outperform the broader indexes during times of uncertainty and volatility. That’s no accident—it’s the result of a disciplined process that starts with quality.

When markets get rocky, investors often rush back to the kinds of companies we’ve been holding all along. Another cornerstone of our strategy is patience. By staying the course and focusing on fundamentals, we’ve been able to grow both our income and capital—even in turbulent times.

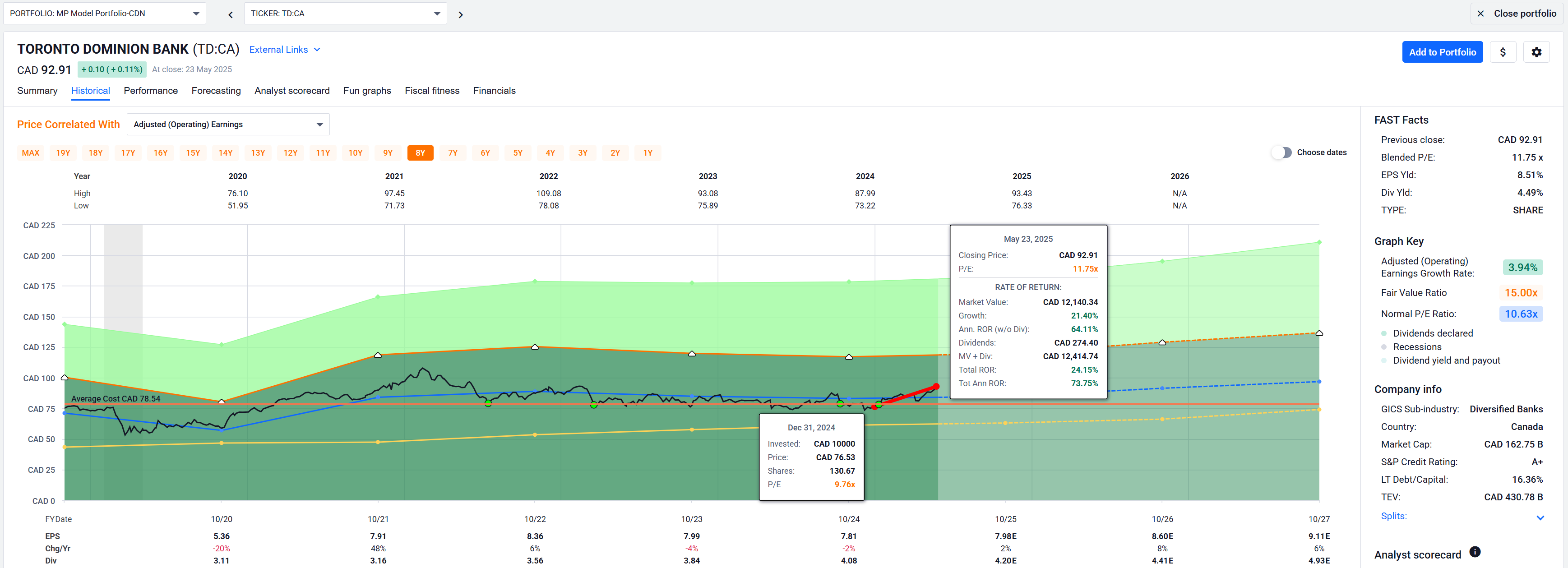

TD Bank reported strong Q1 earnings this past week, and I wanted to highlight it as a great example of the value of patience and conviction in quality businesses. We added to our position in TD over the past couple of years—through the money laundering investigation, the failed First Horizon bid, and the recent trade war. Despite the noise, the fundamentals remained intact, and year-to-date the stock is up ~ 21%. The recent earnings beat was followed by several analyst upgrades, reinforcing our long-term thesis.

The following colours/lines on the FASTgraphs charts shown below represent:

Black line: Price

Yellow line: Dividend Payout Ratio

Orange line: Graham average of usually 15 P/E (price/earnings) for most stocks

Blue line: Normal P/E

Dashed or dotted lines: Estimates only

Green area: Earnings

Green dots: Purchases

Franco-Nevada is another lesson in long-term thinking. We built a full position back in 2022, only to watch the stock price go sideways for a few years when its largest royalty stream—Cobre Panama—was halted in 2023. The mine’s closure was a major blow, but we held on. So far in 2025, the stock has rebounded strongly, and there's renewed optimism that the mine may soon reopen.

Looking ahead, we expect a similar outcome with another of our core holdings: Canadian National Railway. The stock has been trading sideways for the past couple of years, giving us the opportunity to patiently accumulate shares and recently reach our maximum position size. Like many quality companies, CNR's fundamentals have remained solid throughout this period of stagnation, positioning us well for future growth and continued dividend increases.

Wrap Up

We never know how long short-term headwinds will last, but we can usually count on growing dividends and quality businesses bouncing back over time.

Join as a paying subscriber to gain full access to this post and exclusive, subscriber-only content. Plus, get real-time DGI alerts from our model signaling service whenever we make trades in our portfolios. We do the work; you stay in control. Subscribe today and take your dividend growth investing to the next level!

DGI Scorecard

The List (2025)

The Magic Pants 2025 list includes 29 Canadian dividend growth stocks. Here are the criteria to be considered a candidate on ‘The List’:

Dividend growth streak: 10 years or more.

Market cap: Minimum one billion dollars.

Diversification: Limit of five companies per sector, preferably two per industry.

Cyclicality: Exclude REITs and pure-play energy companies due to high cyclicality.

Based on these criteria, companies are added or removed from ‘The List’ annually on January 1. Prices and dividends are updated weekly.

‘The List’ is not a portfolio but a coaching tool that helps us think about ideas and risk manage our model portfolio. We own some but not all the companies on ‘The List’. In other words, we might want to buy these companies when valuation looks attractive.

Our newsletter provides readers with a comprehensive insight into the implementation and advantages of our dividend growth investing strategy. This evidence-based, unbiased approach empowers DIY investors to outperform both actively managed dividend funds and passively managed indexes and dividend ETFs over longer-term horizons.

Note: In the last week of every month, I will show the updated watchlist for our American dividend growers, The List-USA. It will be shown after the Canadian watchlist below.

Performance of 'The List'

Last week, dividend growth stayed the same, with an average return of +6.9% YTD (income).

The price of 'The List' was up from the previous week, with an average YTD return of +6.1% (capital).

Even though prices may fluctuate, the dependable growth in our income does not. Stay the course. You will be happy you did.

Last week's best performers on 'The List' were Franco Nevada (FNV-N), up +5.39%.; TD Bank (TD-T), up +3.43; and Waste Connections (WCN-N) up +2.56%.

Canadian National Railway (CNR-T) was the worst performer last week, down -4.49%.

Off-cycle Q2 earnings reports are still trickling in, with another major bank set to report this week.

In the news section below, you’ll find a thoughtful article highlighting the psychological and emotional benefits of our dividend growth investing strategy—something that often gets overlooked but plays a crucial role in helping investors stay the course.

There’s also a compelling opinion piece on what Berkshire Hathaway could (and maybe should) do next.

Worth a read.