Own the Business, Not Just the Ticker

MP Market Review - May 30, 2025

Summary

Welcome to this week’s MP Market Review – your go-to source for insights and updates on the Canadian dividend growth companies we track on The List! While we’ve expanded our watchlists to include U.S. companies, The List-USA, our Canadian lineup remains the cornerstone of our coaching approach.

Don’t miss out on exclusive newsletters and premium content that will help you sharpen your investing strategy. Explore it all at magicpants.substack.com.

Your journey to dividend growth mastery starts here – let’s dive in!

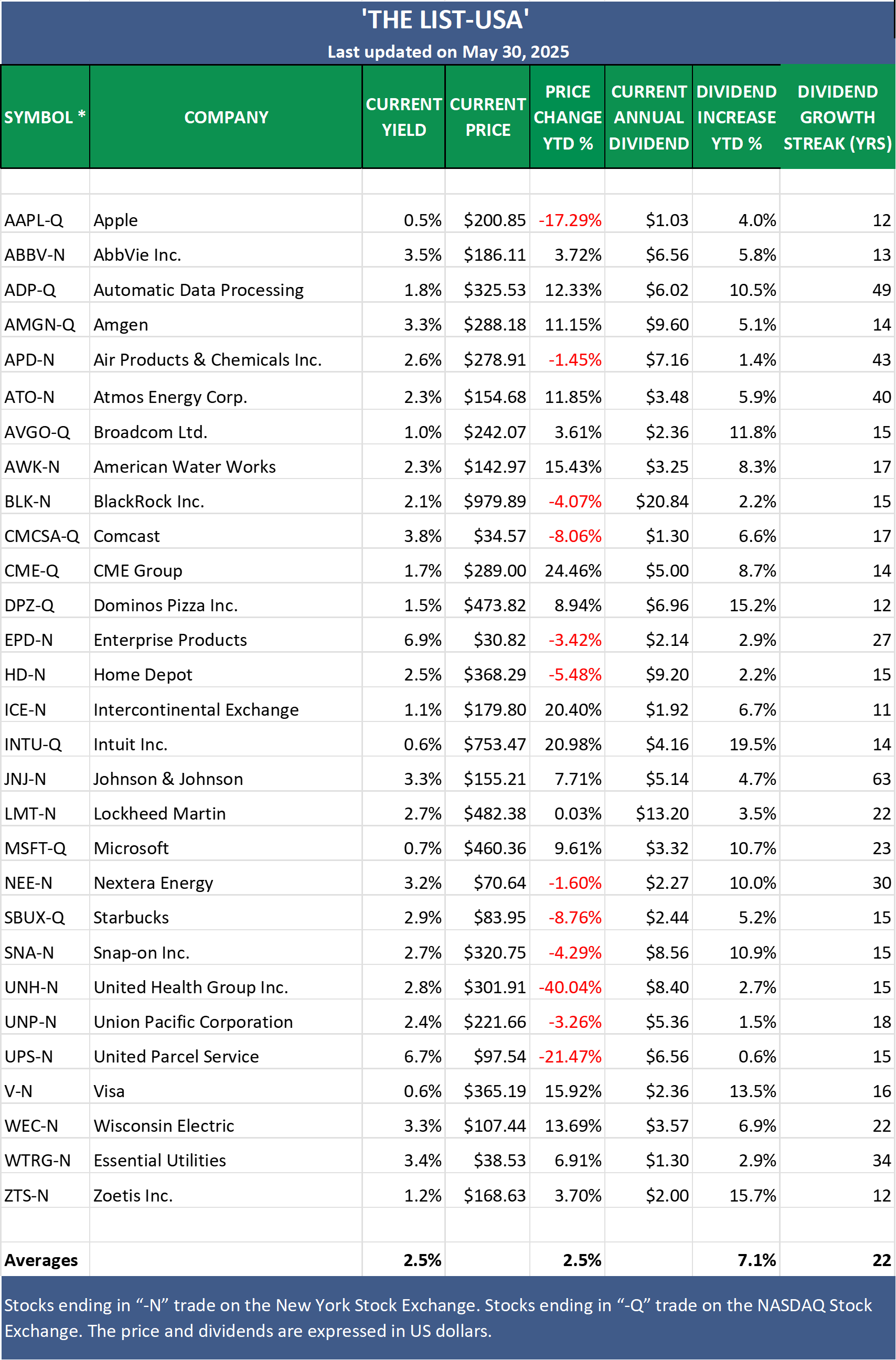

Check out our monthly update on The List-USA below, right after our Canadian version of The List.

Last week, dividend growth of The List stayed the same with an average return of +6.9% YTD (income).

Last week, the price of The List was up from the previous week with an average return of +7.8% YTD (capital).

Last week, there was one dividend announcement from companies on The List.

Last week, there was one earnings report from companies on The List.

This week, one company on The List will report on their off-cycle earnings.

DGI Clipboard

“This is one of the keys to successful investing: focus on the companies, not on the stocks.”

– Peter Lynch

Own the Business, Not Just the Ticker

Intro

Owning the Business, Not Just the Stock

Last week, I sent out the latest performance summaries for our model portfolios. After three years of tracking our journey on the blog, timestamping every trade and documenting each move, it’s rewarding to see the results taking shape. Our capital and income are growing in tandem, and we’re well on our way to outperforming the indexes we track.

At the heart of our strategy is one powerful idea:

We’re not buying stocks. We’re buying businesses.

This ownership mindset shapes everything we do. We treat each investment as though we’re acquiring a meaningful stake in a real company—not just trading a ticker symbol. This mindset keeps us calm during volatility and focused on long-term value, not short-term noise.

It also forces us to go deeper—to truly understand the businesses we own, the quality of their management, and the durability of their cash flows. We focus on North America’s top companies, led by exceptional people and supported by teams of skilled employees. Their success is our success. When they grow, so does our financial freedom.

We don’t see our portfolio as a random collection of stocks. We see it as our personal asset management firm, where our assets are high-quality, dividend-growing businesses. These assets reward us with both rising income and capital appreciation. And because they’re built for the long term, we manage them with a “never sell” mindset.

Over time, we shift from working for our money to having our money work for us. That’s the transition we aim to make, from earners to owners.

Buffett’s Been Doing It For Decades

I recently read an article about the CEO of Coca-Cola, who earned roughly $24 million last year, including bonuses and stock awards.

Meanwhile, Warren Buffett’s Berkshire Hathaway owns 400 million shares of Coca-Cola, which will pay a $2.04 dividend per share this year. That’s more than $800 million in dividends—just for owning the stock.

Buffett didn’t need to run the company. He simply owned a great business and got paid over 30 times more than the CEO.

Next year, he’ll earn even more. Why? Because Coca-Cola has raised its dividend for 62 straight years.

Wrap Up

The lesson?

It’s better to own a great business than to work for one.

Join as a paying subscriber to gain full access to this post and exclusive, subscriber-only content. Plus, get real-time DGI alerts from our model signaling service whenever we make trades in our portfolios. We do the work; you stay in control. Subscribe today and take your dividend growth investing to the next level!

DGI Scorecard

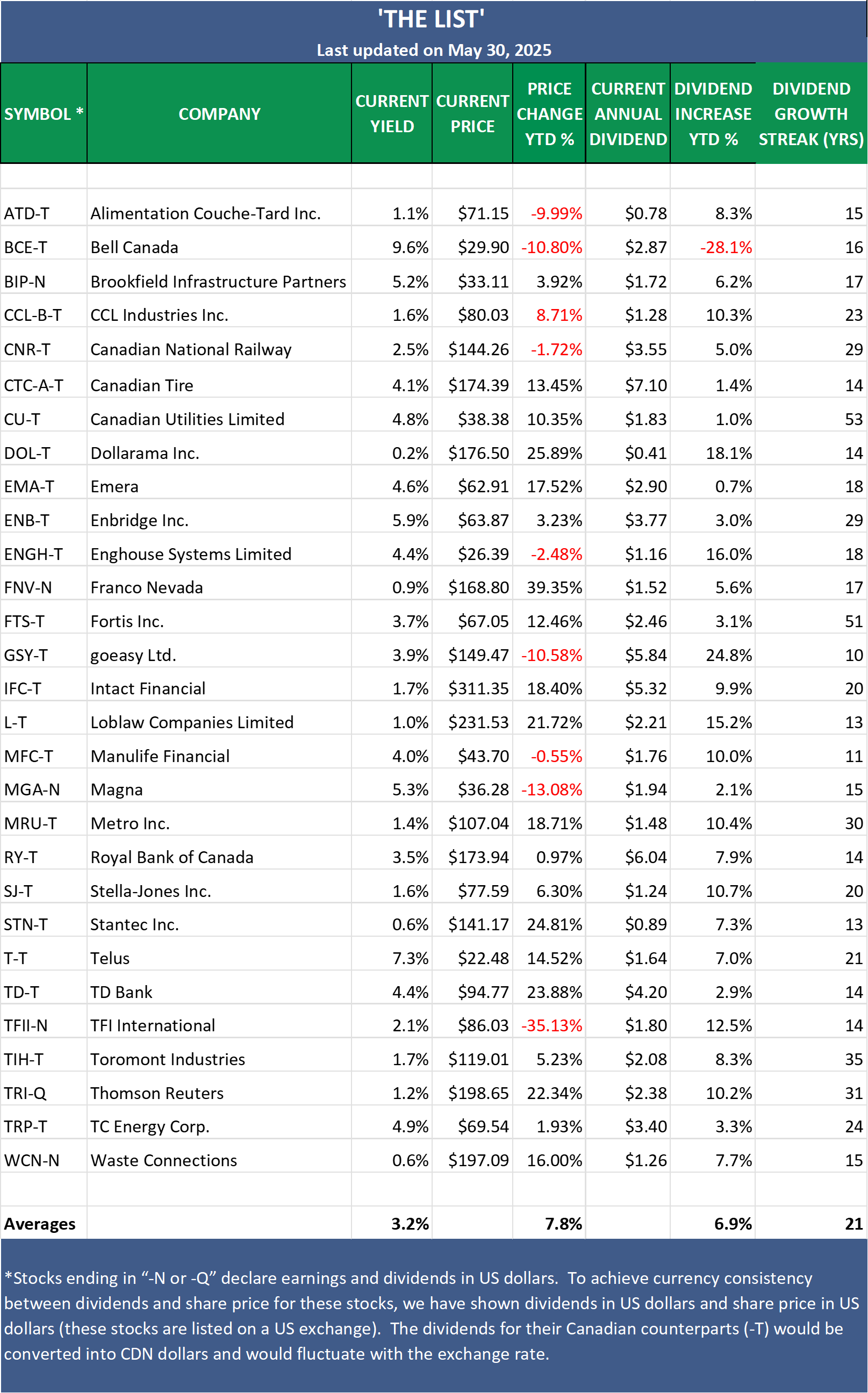

The List (2025)

The Magic Pants 2025 list includes 29 Canadian dividend growth stocks. Here are the criteria to be considered a candidate on ‘The List’:

Dividend growth streak: 10 years or more.

Market cap: Minimum one billion dollars.

Diversification: Limit of five companies per sector, preferably two per industry.

Cyclicality: Exclude REITs and pure-play energy companies due to high cyclicality.

Based on these criteria, companies are added or removed from ‘The List’ annually on January 1. Prices and dividends are updated weekly.

‘The List’ is not a portfolio but a coaching tool that helps us think about ideas and risk manage our model portfolio. We own some but not all the companies on ‘The List’. In other words, we might want to buy these companies when valuation looks attractive.

Our newsletter provides readers with a comprehensive insight into the implementation and advantages of our dividend growth investing strategy. This evidence-based, unbiased approach empowers DIY investors to outperform both actively managed dividend funds and passively managed indexes and dividend ETFs over longer-term horizons.

Note: In the last week of every month, I will show the updated watchlist for our American dividend growers, The List-USA. It will be shown after the Canadian watchlist below.

Performance of 'The List'

Last week, dividend growth stayed the same, with an average return of +6.9% YTD (income).

The price of 'The List' was up from the previous week, with an average YTD return of +7.8% (capital).

Even though prices may fluctuate, the dependable growth in our income does not. Stay the course. You will be happy you did.

Last week's best performers on 'The List' were Canadian Tire (CTC-A-T), up +3.8%; Alimentation Couche-Tard Inc. (ATD-T), up +3.4%; and Loblaw Companies Limited (L-T), up +3.2%.

Royal Bank of Canada (RY-T) was the worst performer last week, down -1.2%.

In the news section below, Tariff tensions may persist, but investors can act, one undervalued bank rises above the rest, and Magna shares, which look attractive despite recent tariff-driven declines.

Worth a read.