Timely Ten: Quality Companies on Sale South of the Border

MP Market Review - June 16, 2026

Summary

This is not a stock-picking newsletter!

It’s a behind-the-scenes look at how a dividend growth portfolio is built, maintained, and improved over time.

Welcome to this week’s MP Market Review.

Before we begin, a quick explanation of the name.

Many years ago, when I first discovered dividend growth investing, I came across a quote that stopped me in my tracks:

“You have a pair of pants. In the left pocket, you have $100. You take $1 out of the left pocket and put it in the right pocket. You now have $101. There is no diminution of dollars in your left pocket. That is one magic pair of pants.”

That is dividend growth investing in its simplest form.

When a quality company pays a dividend, cash moves from the company’s pocket to yours, yet your ownership stake remains intact. As earnings grow, dividends tend to grow. As dividends grow, share prices often follow. Reinvest those dividends into additional shares, and the cycle accelerates: more shares generate more dividends, which buy even more shares.

That’s the magic.

It’s why we call this newsletter Magic Pants Dividend Growth Investing.

Every week, we track the companies on The List, our curated watchlist of Canadian dividend growth businesses selected for their ability to produce rising income over time. While we also publish a U.S. edition each month, Canada remains our primary hunting ground.

Our objective is straightforward:

Grow dividend income by 7-10%+ annually while achieving long-term capital appreciation that matches or exceeds the TSX Composite in Canada and the S&P 500 in the United States.

What follows is not theory.

It is the real-world application of a dividend growth strategy using real money, real positions, and real results.

Markets create an endless stream of noise. We ignore most of it.

Instead, we focus on a handful of metrics that tell us whether our process is working. No predictions. No forecasts. No crystal ball.

Just results.

The magic is in the dividend. Dividends lead. Prices follow.

This Week’s Scorecard

MP Wealth-Builder Model Portfolio (Canada)

Annualized Total Return: +16.46% since inception

Total Return (includes dividends): +11.99% year-to-date

Current Yield: 3.2%

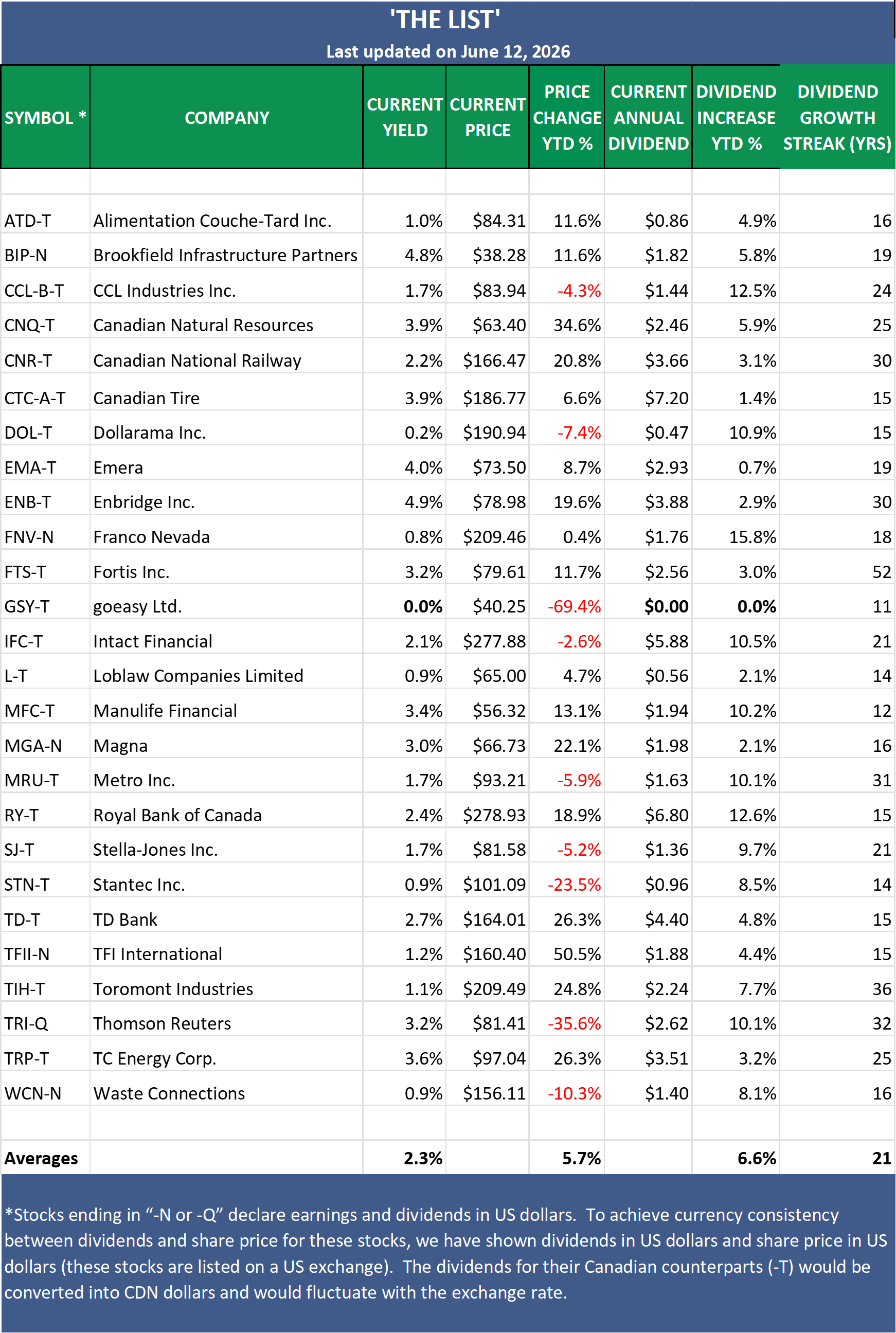

The List (Canada)

Dividend Income Growth: +6.6% year-to-date

Capital Appreciation: +5.7% year-to-date

Dividend Announcements Last Week: None

Earnings Reports Last Week: One

Earnings Reports This Week: None

DGI Clipboard

“Current yield, using its own historic yield as a guide, is, in my view, a fine valuation measure.”

— Tom Connolly

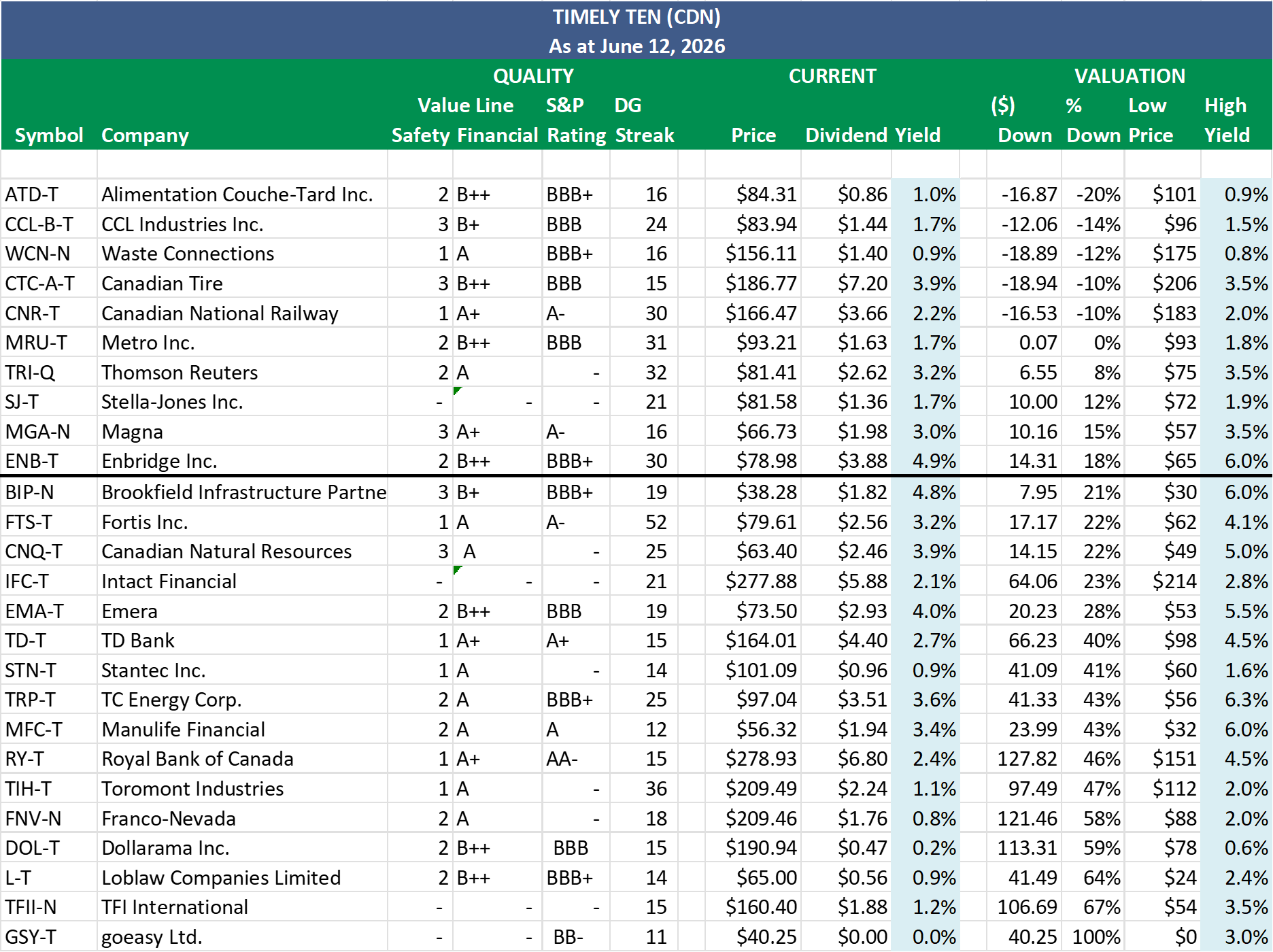

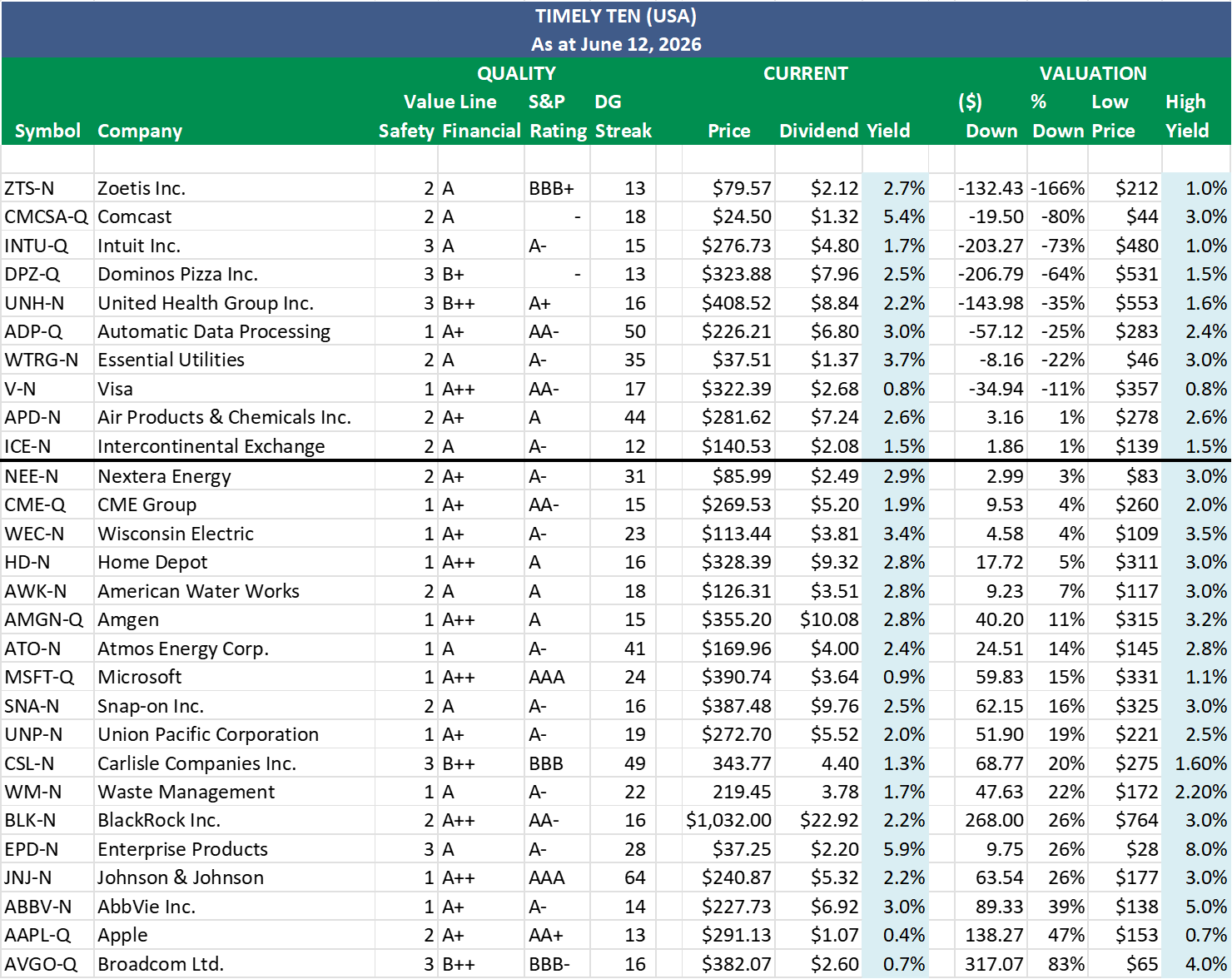

Timely Ten: Quality Companies on Sale South of the Border

There was no change to the Canadian Timely Ten this month. The same ten companies continue to rank as the most undervalued names on our watchlist. What is notable, however, is that nine of the ten stocks actually increased in price over the past month. Only CCL Industries (CCL-B-T) moved lower.

That tells us one thing: value is becoming increasingly difficult to find in the Canadian market. In fact, only the top five companies on the Timely Ten are currently trading above their historical high yields, one of our preferred indicators of undervaluation. By most measures, the Canadian market is looking increasingly frothy.

This is not necessarily a reason to sell quality companies, but it does suggest investors should be increasingly selective when deploying new capital. As dividend growth investors, our objective is not simply to own great businesses, but to own them at sensible prices. When valuations become stretched, future returns often become more dependent on earnings growth and less on multiple expansion. Patience remains an important part of the process.

The American Timely Ten tells a different story. There was considerably more movement up and down the rankings as investors continued to rotate between sectors. Wisconsin Energy (WEC-N) and Home Depot (HD-N) both rallied during the month, pushing them off the list.

Replacing them were two companies already in our American Model Portfolio: Intercontinental Exchange (ICE-N) and Air Products & Chemicals (APD-N). Both experienced share price weakness and have now reached valuation levels that warrant closer attention. While short-term price declines can be uncomfortable, they are often the source of tomorrow’s best long-term opportunities.

One company that continues to intrigue me is Intuit (INTU-Q). The shares have been under significant pressure and climbed further up our undervaluation rankings this month. Intuit now trades at roughly one-third of its historical valuation, a remarkable discount for a business with its quality, competitive advantages, and long-term growth profile.

Whether the market is correctly pricing a slowdown in future growth or simply overreacting to near-term AI concerns remains to be seen. Either way, Intuit is quickly becoming one of the more interesting companies on our American watchlist. As always, we will continue to monitor the fundamentals, dividend growth prospects, and valuation before committing additional capital.

Note: goeasy Ltd.’s dividend has been suspended, so we have moved it to the bottom of the list.

Background

Step three in our process involves regularly monitoring our quality dividend growers, which can become quite challenging depending on the number of companies we track. Fortunately, we rely on ‘The List’ rather than the index’s vast array of stocks, which streamlines our task. Nevertheless, we continually seek methods to enhance our efficiency. Through dividend yield theory, we’ve discovered an approach that has proven remarkably effective in supporting our efforts over the years.

Dividend yield theory is a simple and intuitive approach to valuing dividend growth stocks. It suggests that the dividend yield of quality dividend growth stocks tends to revert to the mean over time, assuming that the underlying business model remains stable. In practical terms, if a stock pays a dividend yield above its ten-year average annual yield, its price will likely increase to return the yield to its historical average. Given that price and yield move in opposite directions, this theory helps us identify stocks poised for a favourable price correction.

We have pre-screened our candidates using the criteria we initially laid out in building our watchlists. This helps us considerably narrow the universe of investable stocks.

Dividend growth streak: 10 years or more.

Market cap: Minimum one billion dollars.

Diversification: Limit of five companies per sector, preferably two per industry.

Cyclicality: Exclude REITs and pure-play energy companies due to high cyclicality.

Next, we rank our Canadian and American watchlists based on how far each stock’s price is below its fair value (Low Price), as determined by dividend yield theory. To find fair value, divide the current dividend (Dividend) by the stock’s historical high yield (High Yield).

Since price and yield move in opposite directions, a lower price results in a higher yield, and vice versa. The ten companies above the thick black line have current prices (Price) below their fair values (Low Price). Put simply, these stocks have a current dividend yield higher than their historical high. According to dividend yield theory, these companies are sensibly priced and have the highest probability of short-term price increases. These are our Timely Ten.

Takeaway

The U.S. market continues to offer a more fertile hunting ground for dividend growth investors. While Canadian opportunities remain limited, an increasing number of quality American businesses are trading at prices that justify further research.

Looking for a helping hand in the market? Members of Magic Pants Dividend Growth Investing get exclusive ideas and guidance to navigate any climate.

The Magic Pants model portfolios (Canadian and American) are real-money, dividend-growth portfolios funded with actual capital and executed in live accounts. Every position shown is owned, sized, and tracked in real time using our disciplined DGI process.

Become a PAID subscriber, and I’ll show you exactly how I do it. In addition, gain full access to this post and exclusive, subscriber-only content. We do the work; you stay in control!

DGI Scorecard

The Magic Pants 2026 list (The List) includes 26 Canadian dividend growth stocks, and our new American watchlist (The List-USA) contains 28 companies. Here are the criteria to be considered a candidate on our watchlists:

Dividend growth streak: 10 years or more.

Market cap: Minimum one billion dollars.

Diversification: Limit of five companies per sector, preferably two per industry.

Cyclicality: Exclude REITs and pure-play energy companies due to high cyclicality.

Based on these criteria, companies are added or removed from ‘The List’ annually on January 1. Prices and dividends are updated weekly.

‘The List’ is not a portfolio but a coaching tool that helps us think about ideas and risk manage our model portfolio. We own some but not all the companies on ‘The List’. In other words, we might want to buy these companies when valuation looks attractive.

Our newsletter provides readers with a comprehensive insight into the implementation and advantages of our dividend growth investing strategy. This evidence-based, unbiased approach empowers DIY investors to outperform both actively managed dividend funds and passively managed indexes and dividend ETFs over longer-term horizons.

Note: In the last week of every month, I will show the updated watchlist for our American dividend growers, The List-USA. It will be shown after the Canadian watchlist below.

Performance of 'The List'

The dividend growth for The List remained unchanged last week, with an average YTD increase of 6.6% (income).

The price of The List was up last week and now stands at +5.7% YTD (capital).

Top Performers Last Week:

Dollarama Inc. (DOL-T), up +5.36%.

Canadian Tire (CTC-A-T), up +4.56%.

Manulife Financial (MFC-T), up +4.30%.

Worst Performer Last Week:

Toromont Industries (TIH-T), down -5.97%.

From breaking news to quarterly earnings reports, we break down the week’s biggest headlines to help you make sense of the market.