Valuation Matters: When Quality Companies Become Expensive

MP Market Review - June 23, 2026

Summary

This is not a stock-picking newsletter!

It’s a behind-the-scenes look at how a dividend growth portfolio is built, maintained, and improved over time.

Welcome to this week’s MP Market Review.

Before we begin, a quick explanation of the name.

Many years ago, when I first discovered dividend growth investing, I came across a quote that stopped me in my tracks:

“You have a pair of pants. In the left pocket, you have $100. You take $1 out of the left pocket and put it in the right pocket. You now have $101. There is no diminution of dollars in your left pocket. That is one magic pair of pants.”

That is dividend growth investing in its simplest form.

When a quality company pays a dividend, cash moves from the company’s pocket to yours, yet your ownership stake remains intact. As earnings grow, dividends tend to grow. As dividends grow, share prices often follow. Reinvest those dividends into additional shares, and the cycle accelerates: more shares generate more dividends, which buy even more shares.

That’s the magic.

It’s why we call this newsletter Magic Pants Dividend Growth Investing.

Every week, we track the companies on The List, our curated watchlist of Canadian dividend growth businesses selected for their ability to produce rising income over time. While we also publish a U.S. edition each month, Canada remains our primary hunting ground.

Our objective is straightforward:

Grow dividend income by 7-10%+ annually while achieving long-term capital appreciation that matches or exceeds the TSX Composite in Canada and the S&P 500 in the United States.

What follows is not theory.

It is the real-world application of a dividend growth strategy using real money, real positions, and real results.

Markets create an endless stream of noise. We ignore most of it.

Instead, we focus on a handful of metrics that tell us whether our process is working. No predictions. No forecasts. No crystal ball.

Just results.

The magic is in the dividend. Dividends lead. Prices follow.

This Week’s Scorecard

MP Wealth-Builder Model Portfolio (Canada)

Annualized Total Return: +16.46% since inception

Total Return (includes dividends): +11.82% year-to-date

Current Yield: 3.2%

The List (Canada)

Dividend Income Growth: +6.6% year-to-date

Capital Appreciation: +5.0% year-to-date

Dividend Announcements Last Week: None

Earnings Reports Last Week: None

Earnings Reports This Week: One

DGI Clipboard

”Once valuations become unusually rich, disappointingly long-term returns are baked in the cake.”

- John Hussman

Valuation Matters: When Quality Companies Become Expensive

Here’s a simple thought experiment. Imagine a business that generated just $50,000 in revenue last year and lost $13,200 in the process. Interested in buying it, you ask the owner what he wants. His answer? A mere $7.5 million.

You’d probably conclude he had completely lost touch with reality. Yet, scaled up, those economics are surprisingly similar to what investors are valuing SpaceX at today. The numbers are vastly larger, but the underlying relationship between sales, losses, and valuation isn’t all that different.

I commented in last week’s newsletter that the Canadian market was beginning to look a little frothy. Valuation remains one of the two pillars of our process, second only to quality.

Throughout the build-out of our Canadian model portfolio, we have been reluctant to sell quality dividend growers unless the underlying business changed, earnings growth slowed materially, or the dividend was cut. That discipline has served us well. One of the biggest mistakes investors make is selling their winners too early. Quality businesses often continue compounding long after they appear expensive.

For investors still accumulating, patience and new contributions usually solve most valuation concerns. But for more conservative investors, or retirees without fresh capital to deploy, there can be a case for trimming positions when they become oversized or when valuations become stretched. Today, three of our largest holdings meet one or both of those criteria.

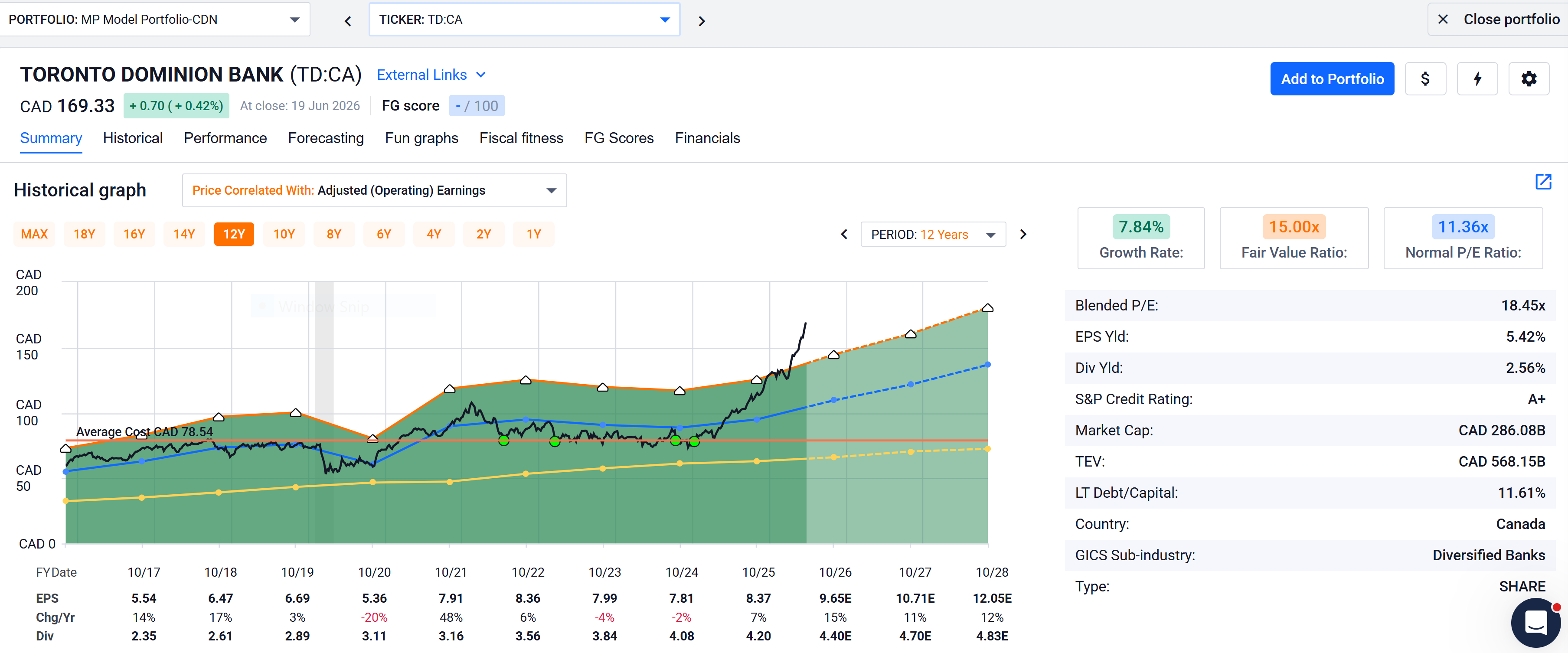

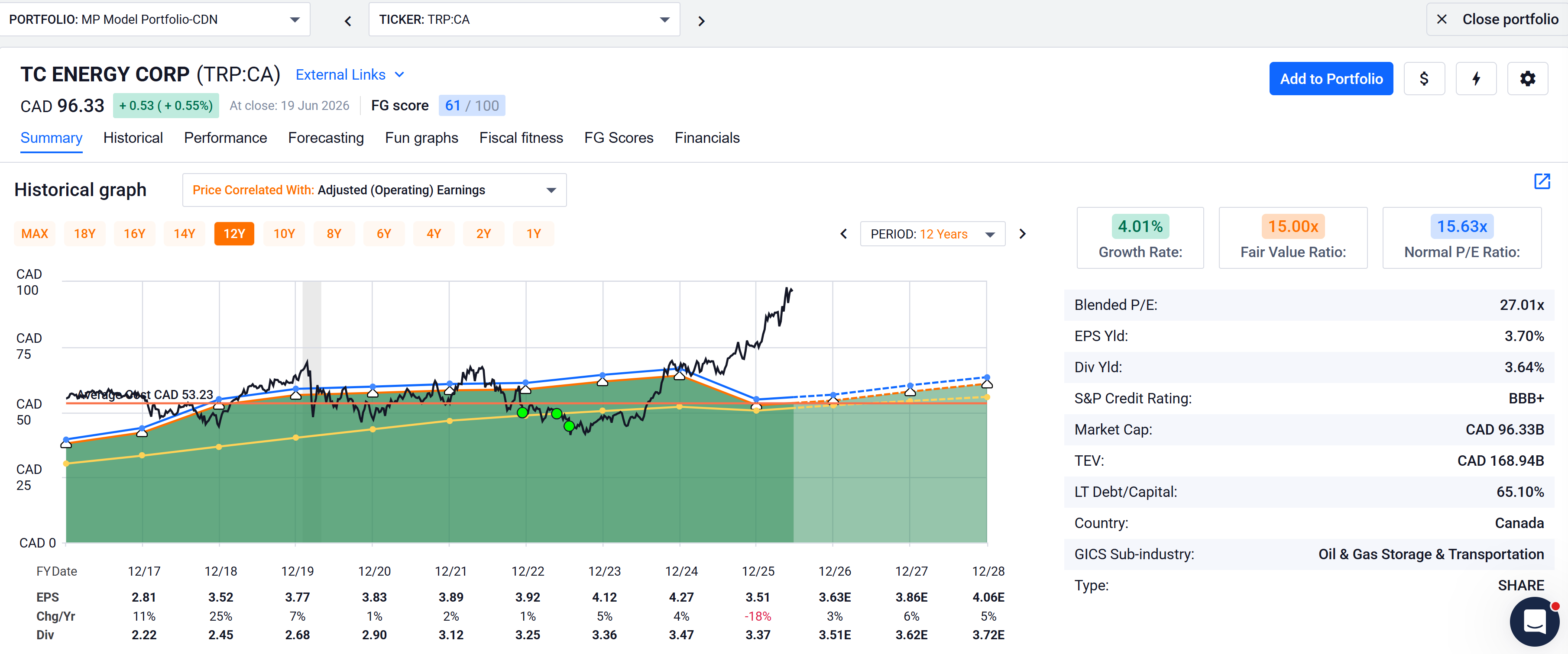

Understanding Valuation

We use FAST Graphs to visualize how companies have historically been valued. Looking back over ten to twelve years allows us to see how the market has priced a business through multiple economic cycles. We prefer buying companies when they are trading within, or below, their normal valuation corridor.

On the charts below:

Black line: Share price

Yellow line: Dividend

Orange line: Fair value (roughly 15 times earnings)

Blue line: Normal historical valuation

Dashed lines: Analyst estimates

Green area: Earnings

Green dots: Purchases

In all three charts, the black price line has moved noticeably above the blue normal valuation line. Historically, these two lines have tended to move much closer together. That doesn’t mean these companies are poor businesses. It simply means investors are currently willing to pay more for each dollar of earnings than they have in the past.

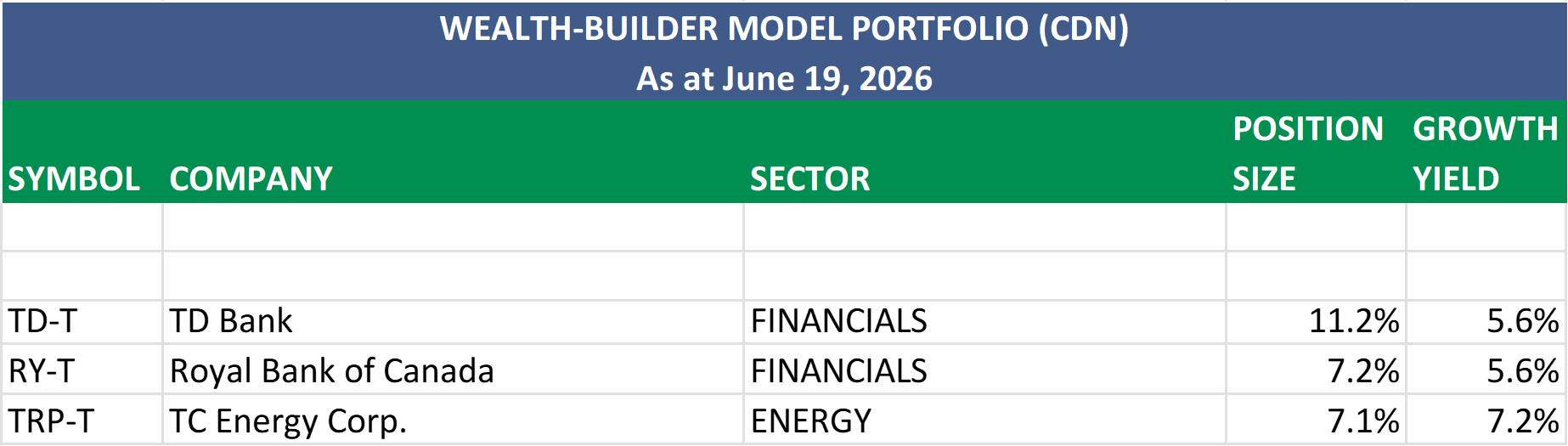

Position Size Matters Too

Our business plan limits core positions to 8% of the portfolio. Toronto-Dominion Bank has grown beyond that level and offers room for trimming. Royal Bank and TC Energy are approaching their maximum allocations, although both still remain within our guidelines.

Despite their richer valuations, all three companies continue to generate growing dividend streams. Their growth yields are well ahead of inflation, and that rising income remains the primary reason we own them.

What Should You Do?

There is no universal answer.

You could trim all three positions back to a 4% weighting and redeploy the proceeds elsewhere. You could simply reduce TD Bank to our 8% maximum and let the others run. You might prefer to raise some cash for an upcoming vacation or maintain dry powder for the next market correction.

Or you may decide to do nothing at all and continue collecting the growing dividends, accepting that short-term price declines are part of the process.

Dividend growth investing (DGI) gives investors options. The beauty of those options is that they are not driven by panic or prediction. They are driven by planning.

Define your approach before markets become emotional. Stick to your process. Judge yourself by long-term outcomes, not short-term fluctuations.

And don’t forget to enjoy the fruits of your portfolio along the way. After all, the purpose of building wealth is not simply to accumulate more money; it is to create more freedom to do the things that matter most.

Takeaway

The goal is not to predict market corrections or sell in panic, but to manage risk thoughtfully and according to a predetermined plan. Whether you choose to trim, hold, or raise cash, the key is to make those decisions deliberately and stay focused on the growing stream of dividend income that quality businesses provide.

Looking for a helping hand in the market? Members of Magic Pants Dividend Growth Investing get exclusive ideas and guidance to navigate any climate.

The Magic Pants model portfolios (Canadian and American) are real-money, dividend-growth portfolios funded with actual capital and executed in live accounts. Every position shown is owned, sized, and tracked in real time using our disciplined DGI process.

Become a PAID subscriber, and I’ll show you exactly how I do it. In addition, gain full access to this post and exclusive, subscriber-only content. We do the work; you stay in control!

DGI Scorecard

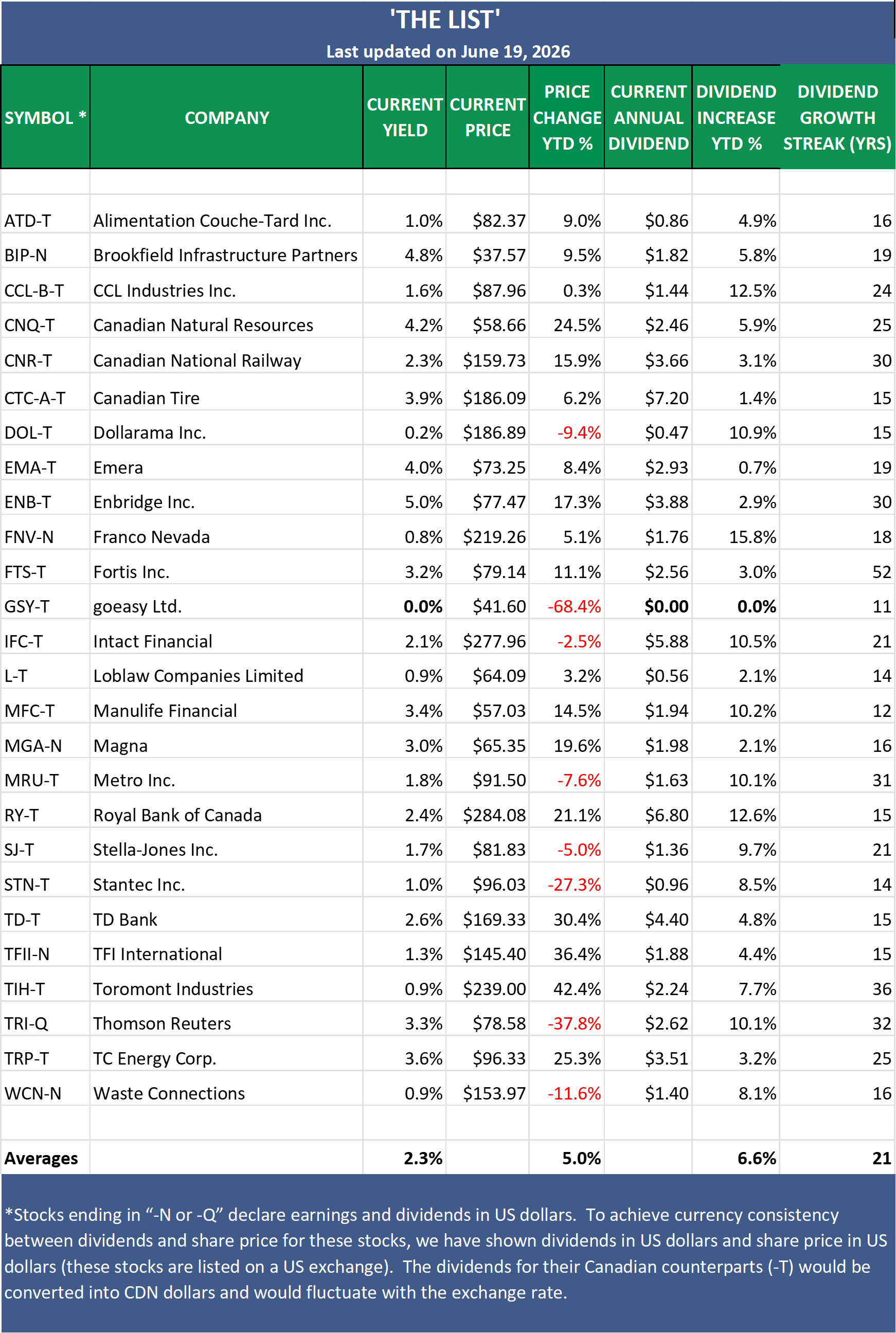

The Magic Pants 2026 list (The List) includes 26 Canadian dividend growth stocks, and our new American watchlist (The List-USA) contains 28 companies. Here are the criteria to be considered a candidate on our watchlists:

Dividend growth streak: 10 years or more.

Market cap: Minimum one billion dollars.

Diversification: Limit of five companies per sector, preferably two per industry.

Cyclicality: Exclude REITs and pure-play energy companies due to high cyclicality.

Based on these criteria, companies are added or removed from ‘The List’ annually on January 1. Prices and dividends are updated weekly.

‘The List’ is not a portfolio but a coaching tool that helps us think about ideas and risk manage our model portfolio. We own some but not all the companies on ‘The List’. In other words, we might want to buy these companies when valuation looks attractive.

Our newsletter provides readers with a comprehensive insight into the implementation and advantages of our dividend growth investing strategy. This evidence-based, unbiased approach empowers DIY investors to outperform both actively managed dividend funds and passively managed indexes and dividend ETFs over longer-term horizons.

Note: In the last week of every month, I will show the updated watchlist for our American dividend growers, The List-USA. It will be shown after the Canadian watchlist below.

Performance of 'The List'

The dividend growth for The List remained unchanged last week, with an average YTD increase of 6.6% (income).

The price of The List was down last week and now stands at +5.0% YTD (capital).

Top Performers Last Week:

Toromont Industries (TIH-T), up +14.09%.

CCL Industries Inc. (CCL-B-T), up +4.79%.

Franco Nevada (FNV-N), up +4.68%.

Worst Performer Last Week:

TFI International (TFII-T), down -9.35%.

From breaking news to quarterly earnings reports, we break down the week’s biggest headlines to help you make sense of the market.